From Dribbles to Dollars: How Okocha’s Financial Discipline Offers Blueprint for Financial Success

September 25, 2025

How FILICON is Building the Foundation for True Economic Freedom, One Nigerian at a Time

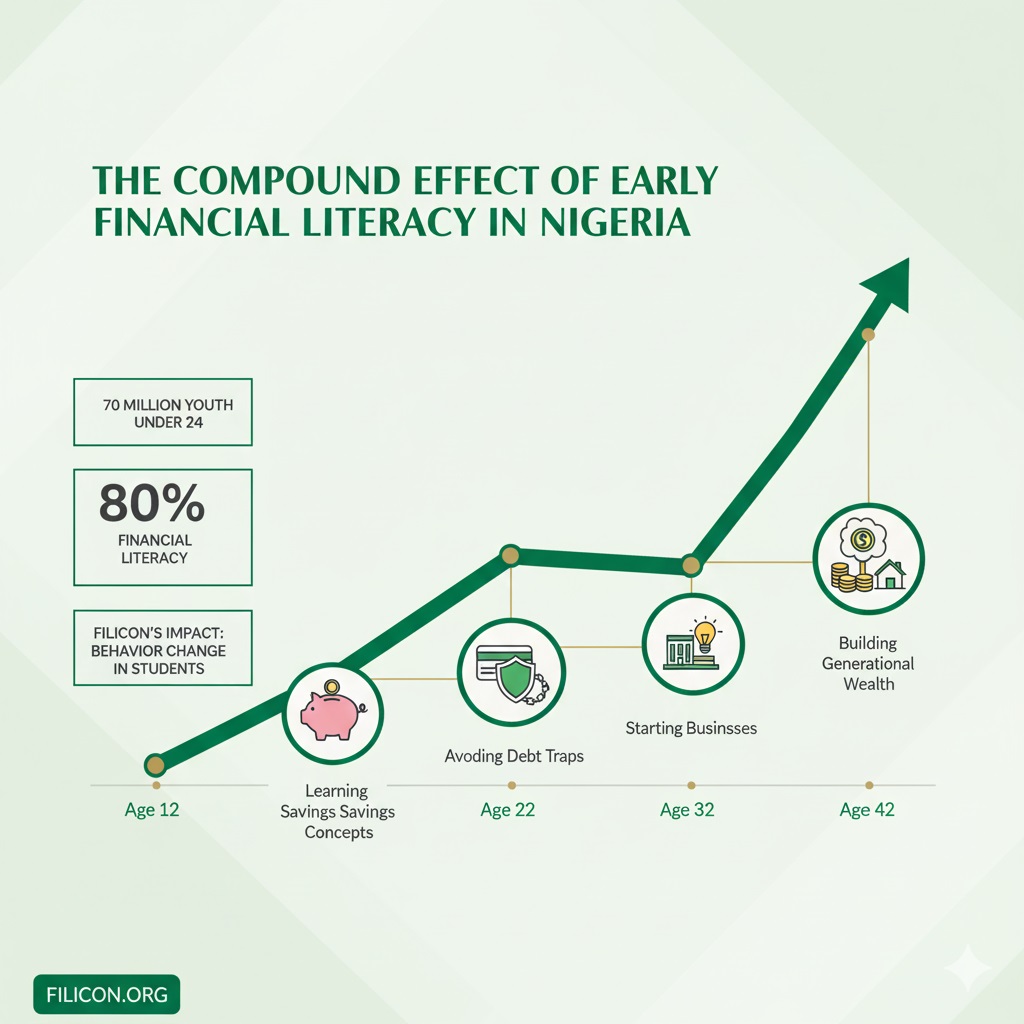

Here’s a truth that keeps me up at night: Nigeria has one of the youngest populations on Earth. Over 70 million young Nigerians under 24. The largest youth demographic in Africa. A population that should be our greatest economic asset.

Yet most of them don’t truly know how money works.

Not because they’re not smart. Not because they’re lazy. But because nobody taught them.

While our young people master TikTok algorithms and navigate Instagram commerce with ease, they’re drowning in get-rich-quick schemes, loan app debt traps, and a financial system that preys on ignorance. We’re raising a generation that knows how to spend digitally but has no idea how to save strategically.

The Financial Literacy Crisis Nobody’s Talking About

The numbers tell a story that should alarm every Nigerian who cares about our future.

India—a country we often compare ourselves to—has only 27% of its adults financially literate. That’s already terrible. But Nigeria? We’re far worse. While exact recent figures are scarce, various studies suggest we hover around 20-26% financial literacy rates. Nearly 8 out of 10 Nigerian adults cannot confidently navigate basic financial concepts like budgeting, interest rates, or investment risks.

Think about what this means: A nation of 200 million people, where the vast majority makes financial decisions in the dark.

Our young people face a perfect storm:

- Digital access without financial education: Smartphones everywhere, but no training on digital financial wellness

- Debt trap apps: Loan platforms that exploit financial ignorance with predatory rates

- Rising consumer culture: Social media creates pressure to spend on appearances while savings accounts stay empty

- Limited upward mobility: Without financial literacy, talent alone won’t break poverty cycles

The cruel irony? Nigeria’s Gen Z is already making money moves. They’re content creators, freelancers, and entrepreneurs. They hustle harder than any generation before them. But hustling without financial intelligence is like running on a treadmill—lots of motion, no forward progress.

Why Financial Literacy Can’t Wait Until “Later”

There’s a dangerous assumption that financial literacy is something people pick up eventually. Maybe in university. Maybe when they get their first job. Maybe when they’re ready to “get serious” about money.

This is wrong. Catastrophically wrong.

Naval Ravikant has a principle: “Specific knowledge is found by pursuing your genuine curiosity.” But before curiosity, there must be exposure. A child who never learns that money can work for them—through compound interest, strategic saving, or entrepreneurship—will never develop curiosity about wealth building. They’ll only learn consumption.

Consider this: By the time most Nigerians receive any financial education (if they ever do):

- They’ve already formed habits.

- They’ve already internalized money scripts from parents and influencers who themselves lacked financial literacy.

- They’ve already made costly mistakes. (Read this twice).

Early financial literacy isn’t just beneficial—it’s the foundation upon which everything else is built.

The Multi-Pronged Approach That Actually Works

Global evidence shows us what works. Brazil integrated financial literacy into school curricula. Australia made it a core competency. The results speak for themselves: young people who learn financial concepts early make better decisions for life.

But here’s what many miss: Financial literacy education must be multi-dimensional.

1. Schools as the Primary Battleground

Every Nigerian child should learn financial literacy alongside English and Mathematics. Not as an abstract subject, but as a practical life skill. Budgeting. Saving. Understanding debt. Recognizing scams. Basic investment concepts.

When you teach a child to read, you give them access to knowledge. When you teach them financial literacy, you give them access to wealth creation.

2. Technology as the Equalizer

Nigeria has over 100 million internet users. Youth smartphone penetration is exploding. This isn’t a problem—it’s an opportunity.

Gamified learning platforms. Interactive storytelling. Mobile apps that make financial education engaging rather than boring. Technology can take financial literacy from Lagos to rural Sokoto, from Abuja to remote villages in Ebonyi.

The same phone that tempts young people with consumerism can be the tool that teaches them to build wealth.

3. Community-Based, Peer-to-Peer Learning

Financial literacy thrives in conversation. When young people discuss money with peers and families, concepts move from abstract to concrete. Community interventions create ripple effects—one financially literate student influences siblings, parents, neighbors.

This is where grassroots initiatives shine.

Enter FILICON: The Intervention Nigeria Desperately Needs

This is where the story gets hopeful.

While government policy moves slowly and traditional education systems struggle to adapt, a movement emerged. The Financial Literacy Club of Nigeria (FILICON) isn’t waiting for permission or perfect conditions. We’re on the ground, in schools, changing lives right now.

FILICON’s model mirrors the most successful global interventions, but with Nigerian context baked in:

Making Money Relatable Through Stories

Drawing inspiration from proven international projects, FILICON uses storytelling to make financial concepts stick. Not dry lectures about compound interest—but narratives young Nigerians can see themselves in. Stories about students making smart money choices. Tales about avoiding debt traps. Examples drawn from Nigerian daily life.

Because here’s what Ann Handley understands that most education initiatives miss: People don’t remember facts. They remember stories.

Structured Learning That Shifts Behavior

FILICON isn’t just teaching theory. We’re measuring impact. Students begin understanding structured money management—needs, wants, and savings. The classic 50/30/20 rule, adapted for Nigerian realities.

Post-intervention data shows remarkable shifts:

- Students moving from “spend everything” mindsets to structured allocation

- Increased focus on education savings over immediate gratification

- More frequent family financial conversations

That last point is crucial. When a child learns financial literacy, they don’t just change their future—they influence their present household. Parents start talking about money with intention. Siblings learn by osmosis. Financial wellness spreads.

Digital Tools Meet Ground Reality

FILICON leverages technology without becoming enslaved to it. Mobile learning modules complement in-person workshops. Interactive content meets community engagement. The approach scales without losing the human touch.

This is critical in Nigeria, where infrastructure is uneven and digital literacy varies. FILICON meets young people where they are, not where we wish they were.

Building Confidence, Not Just Knowledge

Here’s something most financial literacy programs overlook: Information without confidence is useless. Young people need to believe they can manage money well, not just know concepts.

FILICON’s model builds this confidence through practice, repetition, and early wins. Students don’t just learn about saving—they experience the satisfaction of reaching a savings goal. They don’t just hear about budgeting—they create actual budgets and see them work.

Confidence compounds. A student who successfully manages ₦5,000 gains courage to manage ₦50,000 later. Then ₦500,000. Then more.

The Ripple Effect Is Already Happening

Let’s be specific about impact. Because in the content world David Ogilvy built, specificity sells—not hype.

Early FILICON interventions show:

- Behavioral change at scale: Students adopting structured money management frameworks they’ll carry for life

- Goal orientation shift: Young people choosing education and long-term financial security over short-term wants

- Household conversations increasing: Financial discussions within families rising by significant margins post-intervention

- Confidence metrics improving: Students reporting greater comfort discussing and managing money

But the real magic isn’t in the immediate metrics. It’s in the compounding effect.

A financially literate 12-year-old doesn’t just make better decisions at 12. They make better decisions at 22. At 32. At 42. They avoid debt traps in their 20s. They start businesses in their 30s. They build generational wealth in their 40s.

Multiply this across thousands of students. Then tens of thousands. Eventually hundreds of thousands.

This is how you change a nation’s economic trajectory—one financially empowered young person at a time.

Why This Matters More Than You Think

Nigeria stands at a crossroads.

We can continue down the path we’re on—where financial illiteracy keeps brilliant minds trapped in cycles of poverty, where hustle culture replaces strategic planning, where the only financial advice young people receive comes from scammers, predatory financial institutions, and loan sharks.

Or we can choose a different path.

Financial literacy isn’t sexy. It doesn’t make headlines like fintech funding rounds or crypto bull runs. But it’s the foundation everything else is built on.

You cannot build a financially inclusive society on financially illiterate people.

All the mobile banking apps, all the digital wallets, all the investment platforms in the world won’t matter if people don’t understand how to use them wisely. Financial inclusion without financial literacy is just giving people more ways to get into debt.

FILICON understands this. We’re not building flashy solutions that look impressive in pitch decks. We’re doing the unglamorous, essential work of actually educating young Nigerians, professionals and executives alike.

This is bottom-up economic empowerment. Not waiting for government. Not waiting for perfect conditions. Not waiting for someone else to solve it.

The Urgent Call to Action

If you care about Nigeria’s future, you should care about financial literacy. This is what can birth true freedom from modern financial slavery both at the personal and national levels.

The future belongs to those who build it. FILICON is building it. The question is whether you’ll be part of the building or just watch from the sidelines.

If you’re an educator: Integrate financial literacy into your teaching. Partner with FILICON. Make it a priority, not an afterthought.

If you’re a parent: Talk to your children about money. Often. Honestly. Don’t pass on your financial traumas—break the cycle.

If you’re a tech builder: Create tools that make financial literacy engaging. Gamify it. Make it social. Make it accessible.

If you’re a policymaker: Make financial literacy mandatory in schools. Fund and support programs like FILICON. Measure outcomes. Scale what works.

If you’re a young Nigerian, a graduate or even a business executive: Seek out financial education aggressively. Join FILICON. Your future self will thank you. Your children will thank you. Your grandchildren will thank you.

The Bottom Line

Nigeria’s greatest asset isn’t our oil. It isn’t even our numbers. It’s the potential within our young people.

But potential without knowledge is just possibility. Financial literacy transforms possibility into reality.

FILICON isn’t saving the day because we’re heroes. We’re saving the day because we showed up, did the work, and refused to wait for someone else to solve the problem.

The question now is: Will you join us?

Because here’s the truth we should all agree on: The best time to start was yesterday. The second-best time is now.

Nigeria’s next generation doesn’t need another speech about how they’re the future. They need tools, knowledge, and confidence to actually build that future.

FILICON is providing exactly that.

And this—this quiet revolution in financial literacy—might just be the most important work happening in Nigeria today.

Visit FILICON.ORG to learn more, support the mission, or bring financial literacy programs to your community. Because every financially literate young Nigerian is an investment in our collective future.

{kind=link}

{kind=link}

{kind=link}